The COVID-19 pandemic has caused approximately one million deaths in the United States and continues to impact our daily life. Since the beginning of the COVID-19 pandemic in early 2020, we now have much more insight into COVID-19 deaths in the US, including hopes for how the pandemic may wind down because of widespread vaccinations and protection generated from prior infections.

While the media has reported how COVID-19 impacts the elderly the most, the data provided by the Centers for Disease Control and Prevention (CDC) may be telling us a more insightful story for middle-aged and younger individuals on the relative to expected mortality rate basis. As such, the experience over the past two years may be instructive for the life insurance industry going forward.

Excess mortality vs. “normal”

To determine the excess mortality during the COVID-19 pandemic, we utilized the general population data provided by the CDC for our analysis. Currently, the CDC has provided the final official data for 20201 and the provisional data for 20212.

Mortality data used in our analysis are based on all causes of death (not just COVID-19), as the COVID-19 pandemic is impacting the population both directly and indirectly. Though some of these extra deaths were not directly linked to COVID-19 (i.e. not coded as COVID-19 deaths), they may be ascribed to the broader effects of the pandemic, including the societal stress from lockdowns and unemployment, and the pandemic stress both on hospitals’ ability to serve and on sick people’s willingness to go to the hospital.

For our analysis, we define “normal” mortality to be the average mortality of 2017-2019. The following graphs show the excess mortality in 2020 and 2021 versus the “normal” mortality by age group. We first show the deaths with COVID-19 listed as the underlying cause on the death certificate as a percentage of the normal mortality, and then remaining excess deaths are shown as non-COVID deaths.

2020 Male mortality increase (%) over “normal”

2020 Female mortality increase (%) over “normal”

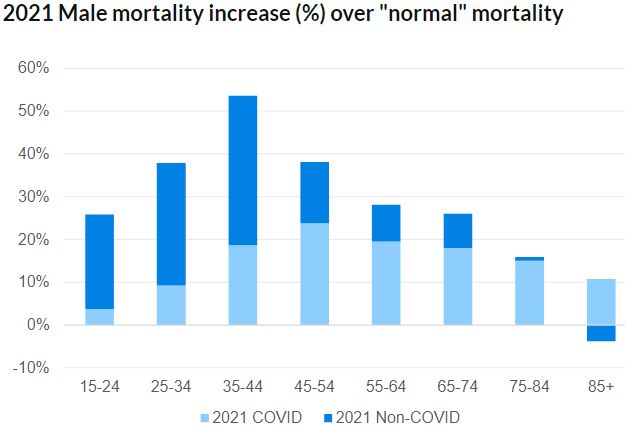

2021 Male mortality increase (%) over “normal”

2021 Female mortality increase (%) over “normal”

The press may have reported that the majority of COVID-19 deaths were among the elderly (which is certainly true on an absolute count basis), but there has been limited discussion about the increased mortality risk relative to the expected level of mortality at all adult ages. Obviously, these relative increases are particularly important for insurers, which price for and hold reserves based on mortality rates that vary by age.

While the overall percentages of total mortality increase (vs. “normal”) were near 18% for 2020 and 20% for 2021, the percentage of total mortality increase for different age groups could be significantly different depending on the time elapsed since the pandemic, with a wide range of 4% to 54%. As shown in the above graphs, in both 2020 and 2021, the total relative mortality increase peaks in the 35-44 age group for both males and females. In general, smaller total relative mortality increases were experienced in the older age groups.

In 2020, the relative increase in mortality attributable to COVID-19 was fairly consistent for middle-aged people and the elderly. However, the relative increase in mortality attributable to COVID-19 in 2021 was materially higher for middle-aged people compared to the elderly.

While COVID-19 was one of the main medical causes of increased mortality during the pandemic, the impact of societal changes as a response to the pandemic (e.g. societal stress, delayed healthcare) should also be considered when evaluating the overall mortality impact from the pandemic. These deaths attributable to these societal changes have caused a significant relative increase in the mortality rates of the younger age groups. For example, deaths caused by drug overdose increased by more than 35% during the pandemic for the age group of 35-44.

While slightly higher for younger age groups, in 2020 the total relative mortality increase per age group is relatively steady across age groups. We suspect that there were fewer societal differences between the age groups contributing to the excess levels of mortality in 2020. However, in 2021, the differential is much higher. While the virus may have been similarly lethal by calendar year, there were significant societal differences.

- In 2021, the vaccine became available, first to older-aged people, but then soon after to everyone. Vaccination rates for older-aged people are higher than for younger individuals.

- By 2021, younger and middle-aged people were becoming more comfortable in public settings compared to elderly individuals. As such, younger and middle-aged people may have been more exposed to the virus (as per the comment above, with a lower chance of being vaccinated).

- By 2021, we learned how to prevent catastrophic spreading in nursing homes, which was a significant contributor to the levels of elderly excess mortality in 2020. We also learned more about how to mitigate spreading in general (e.g. being outdoors).

- The cumulative financial and social implications of the lockdowns may have also had a significant impact on the non-COVID relative mortality increase in young and middle-aged people compared to the elderly.

- Medical treatment for the disease also improved by 2021, but it is not clear why that would lead to differences across age groups. One hypothesis is that older people were more inclined to be in communication with their medical professionals soon after being diagnosed with COVID-19 while there still was an opportunity for successful treatment.

Implications and considerations

While COVID-19 has not yet finished running its course, we now have more experience to assess the impact of the COVID-19 pandemic on the life insurance industry. There is no doubt that the COVID-19 pandemic has been impacting the insurance industry in many ways (e.g. product development, assumption setting, economic capital). It’s important to consider and understand the potential implications of the COVID-19 pandemic to the industry and the changes life insurers need to consider as a result of the COVID-19 pandemic.

- Mortality assumptions. Mortality rates across all adult ages have been significantly higher since the beginning of the COVID-19 pandemic. However, there may be a mixture of push-pull effects on the mortality from the near to long term:

- There may be some chronic complications from COVID-19 infection (“Long COVID”), which may result in people “aging” faster than if they weren’t infected with COVID-19. Long COVID may turn out to be a substantive phenomenon and, in turn, may cause future mortality rates to be higher than otherwise expected.

- Many people delayed elective healthcare, which may have led to reduced diagnoses of conditions (either delayed or missed entirely). This dynamic may cause future mortality rates to be higher than otherwise expected.

- However, it is possible that COVID-19 may have mostly accelerated deaths from people in poor health already who may have otherwise died earlier than the average person in their age group. Colin Powell, former U.S. Secretary of State, may be a noteworthy example of this – he died with COVID-19, but was suffering from cancer, and COVID-19 may have accelerated his death, which otherwise may have been caused by his cancer within a year or two. We may see a scenario in which the “strong survived” may cause future mortality rates to be lower than expected, thus leading to higher levels of mortality improvement.

- Pandemic modeling and economic capital. We had envisioned the 1918 influenza pandemic as approximately a one-in-400-year event, but now the COVID-19 pandemic has shown a level of excess mortality comparable to that from the 1918 influenza pandemic. Thus, we have had two pandemics with similar severity in the last 100 to 105 years, so frequency estimates may need to be updated. The question we must ask is whether we view it as one pandemic in each of the last two 100-year periods (suggesting a frequency around 1% per year), or could we consider two pandemics in the last 100 years (suggesting a frequency higher than 1% per year)? This could be an essential consideration in catastrophic modeling and capital requirements.

- Mergers and acquisitions (M&A) and reinsurance. Buyers of life insurance and annuity blocks of business are considering the implications of the pandemic and how future experience may unfold. Further, life insurers are considering exposures to mortality risk in light of what was experienced under the pandemic.

- Long-term care (LTC) and annuity living benefits. While the COVID-19 pandemic increased life insurance claims, at the same time, it may have reduced liabilities for payout annuities, long-term care and disability income claims, as well as the living benefit claims associated with fixed and variable annuities. While those types of business may have benefited over the last couple of years from higher levels of reserves released than expected, companies may want to examine the implications of higher levels of mortality improvement if we follow with a “strong survived” scenario.

- Pricing, product development, and underwriting. Clearly, the implications on assumptions and economic capital will ultimately impact pricing. However, the industry should examine how changed attitudes from the pandemic may impact people’s views of insurance products, which in turn can have implications for effective product design. Also, the unknown long-term chronic complications from COVID-19 infections may create challenges for accurate underwriting – for example, should insurers begin to ask about potential insureds medical history with COVID-19?

- Sales. Life insurance sales may have increased due to higher awareness of life insurance protection needs raised by the COVID-19 pandemic. According to LIMRA, 31% of consumers said they were more likely to buy insurance due to the pandemic3. The potential increased need for life insurance (especially among younger people) may have created an opportunity for insurers to boost sales. However, this dynamic may reverse as the impact of the pandemic lessens. If so, insurers will have to develop alternative strategies to drive sales growth.

- Sensitivities. As more experience and data unfolds, companies may want to consider various sensitivities to assess the potential financial impacts from future pandemics.

- Mental health. The COVID-19 pandemic not only impacted people’s physical health but also their mental health. While the pandemic increases the general population’s mortality rates, it may also increase mental health-related deaths caused by the stress from the COVID-19 pandemic, e.g., suicide, drug overdoses, etc. While the overall suicide rate declined during the pandemic, deaths caused by drug overdoses increased significantly. Consideration should be given to how a more anxious population may influence future mortality rates.

Conclusion

While the media has reported that the COVID-19 pandemic mostly affected older aged people, the data shows that there was an elevated level of relative mortality increase across all age groups, including the main age groups that own life insurance. As we look back on the last couple of years, we collectively have learned a lot about disease, pandemics, and the implications on society. Though insurers may have different experiences from the general population, it is important for the life insurance industry to learn from the experience and make sound decisions for the many implications of how COVID-19 will affect the industry going forward.

This article was first published at https://www.milliman.com/en/insight/How-does-COVID-19-impact-the-life-insurance-industry-going-forward#. Re-used with permission.

References

1 CDC. Multiple Cause of Death, 1999-2020 Request. Retrieved March 6, 2022, from https://wonder.cdc.gov/mcd-icd10.html.

2 CDC. Provisional Mortality Statistics, 2018 Through Last Month Request. Retrieved March 6, 2022, from https://wonder.cdc.gov/mcd-icd10-provisional.html.

3 LIMRA (March 23, 2022). LIMRA: Challenges Brought On by the Pandemic Highlight the Importance of Family. Retrieved May 19, 2022, from https://www.limra.com/en/newsroom/industry-trends/2022/limra-challenges-brought-on-by-the-pandemic-highlight-the-importance-of-family/#:~:text=According%20to%20LIMRA’s%20and%20Life,highest%20growth%20recorded%20since%201983.